Kinder Morgan Dividends: Is KMI a Safe Income Investment?

Consistent Dividend Growth with Competitive Yield

Kinder Morgan (NYSE: KMI) has long been a popular choice among income-focused investors, thanks to its attractive dividend yield and stable cash flow. But beyond just yield, what makes KMI particularly appealing is its consistent dividend growth over recent years — a trait that’s essential for long-term income investing.

KMI operates one of the largest energy infrastructure networks in North America, including pipelines and storage facilities for natural gas, crude oil, and CO2. This stable, fee-based business model generates predictable cash flows, which in turn support its dividend payouts. As of 2024, Kinder Morgan offers a dividend yield of around 6%, which is notably higher than the S&P 500 average. This makes it competitive not only among energy stocks but also across broader income-generating investments.

What’s even more reassuring is the company’s commitment to growing its dividend. Since restructuring its dividend policy in 2016, Kinder Morgan has steadily increased its annual dividend. In its latest earnings report, the company announced a dividend increase, marking another year of consistent growth — a positive signal for investors seeking both income and stability. [Source: Kinder Morgan Investor Relations](https://ir.kindermorgan.com/)

Moreover, KMI maintains a conservative payout ratio and focuses on maintaining strong coverage of its dividend through distributable cash flow (DCF). This approach reduces the risk of dividend cuts, even during volatile market conditions. For investors looking for a relatively safe income stream with the potential for modest growth, Kinder Morgan stands out as a solid candidate.

In summary, KMI’s combination of a high yield, consistent dividend growth, and a stable business model makes it a compelling option for income investors. As always, it’s wise to consider how this fits into your broader portfolio and risk tolerance, but for many, Kinder Morgan offers a dependable source of passive income.

Resilient Revenue from Long-Term Pipeline Contracts

Kinder Morgan (KMI) is one of the largest energy infrastructure companies in North America, and its dividend appeal lies in the stability of its cash flows. A key reason for this stability is the company’s reliance on long-term, fee-based contracts for its pipeline operations. These contracts typically span 10 to 20 years and are structured to provide steady revenue regardless of short-term fluctuations in commodity prices.

This business model helps insulate Kinder Morgan from the volatility often seen in the energy sector. Instead of depending on oil and gas prices, the company earns predictable income from transporting energy products for its customers. Most of these customers are investment-grade counterparties, which further reduces credit risk.

For income-focused investors, this means Kinder Morgan can maintain and even grow its dividend payouts with greater confidence. The company’s distributable cash flow (DCF), a key metric for dividend sustainability, has remained robust even during downturns in the energy market. In fact, according to Kinder Morgan’s 2023 annual report, approximately 68% of its earnings before interest, taxes, depreciation, and amortization (EBITDA) came from take-or-pay or fee-based contracts.

In addition, Kinder Morgan has shown a disciplined approach to capital allocation, prioritizing dividend coverage and debt reduction over aggressive expansion. This conservative financial strategy adds another layer of security for dividend investors.

If you’re considering Kinder Morgan as a dividend stock, its long-term contracts provide a strong foundation for reliable income. However, always remember to assess the broader energy market and regulatory risks before making investment decisions.

For more detailed financials and contract structure, you can refer to Kinder Morgan’s official investor relations page: https://ir.kindermorgan.com

Key Risks and Recent Quarter Performance Review

Kinder Morgan (KMI) is a well-known name among income investors, primarily due to its attractive dividend yield. However, before considering it a safe income investment, it’s essential to evaluate both the risks involved and its recent financial performance.

Let’s start with the key risks. One of the most significant concerns with Kinder Morgan is its exposure to commodity price volatility. Although the company operates primarily through fee-based contracts, prolonged periods of low natural gas and oil prices can indirectly affect its cash flows and future growth prospects. Another notable risk is its high debt load. As of the latest quarter, Kinder Morgan carries over $30 billion in long-term debt. While the company has made efforts to reduce leverage over the years, interest rate hikes can increase debt servicing costs, potentially pressuring dividend sustainability.

Regulatory and environmental risks also play a role. As a pipeline operator, Kinder Morgan must navigate complex federal and state regulations. Any delays or denials in project approvals can hinder expansion plans and impact revenue growth.

Now, let’s review the recent quarter’s performance. In Q1 2024, Kinder Morgan reported adjusted EBITDA of $1.97 billion, a slight increase from the previous year. Distributable cash flow (DCF) stood at $1.37 billion, comfortably covering its dividend payout. The company reaffirmed its full-year guidance, projecting a dividend of $1.13 per share for 2024, representing a modest increase from 2023. This consistency is reassuring for income-focused investors.

Despite these positives, it’s important to keep an eye on macroeconomic trends and energy sector dynamics. Investors should also monitor how effectively Kinder Morgan manages its capital expenditures and maintains its dividend coverage ratio.

For a deeper dive into Kinder Morgan’s financials, you can visit their official investor relations page: https://ir.kindermorgan.com/

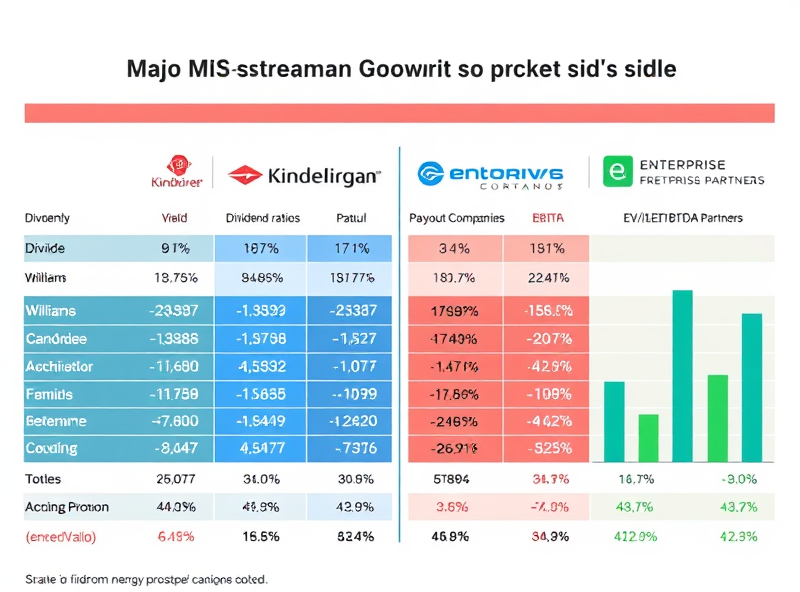

Peer Comparison and Market Valuation Insights

When evaluating Kinder Morgan (KMI) as a dividend stock, it’s essential to compare it with its peers and understand how the market currently values the company. This helps investors determine whether KMI offers a compelling income opportunity relative to similar companies in the energy infrastructure sector.

Kinder Morgan operates in the midstream energy space, alongside peers like Enbridge (ENB), Williams Companies (WMB), and Enterprise Products Partners (EPD). Compared to these companies, KMI offers a competitive dividend yield—currently around 6.3% as of early 2024. While this is slightly lower than EPD’s yield, it is higher than WMB’s and comparable to ENB’s. However, dividend yield alone doesn’t tell the full story.

One key metric to consider is the payout ratio. KMI maintains a relatively conservative payout ratio, which indicates that its dividend is well-covered by distributable cash flow. This is crucial for income investors seeking stability. In contrast, some peers may offer higher yields but with higher payout ratios, potentially signaling greater risk if cash flows decline.

From a valuation standpoint, KMI trades at a forward EV/EBITDA multiple of approximately 8.5x, which is in line with the industry average. This suggests that the stock is fairly valued relative to its earnings potential. Investors should also note that KMI has been actively managing its debt levels and capital expenditures, positioning itself for sustainable long-term growth.

In summary, Kinder Morgan holds its ground well against its peers in terms of dividend yield, payout safety, and valuation. For income-focused investors, KMI represents a balanced choice with a strong track record and prudent financial management.

For more detailed financial data and peer comparisons, you can refer to the official Kinder Morgan investor relations page: https://ir.kindermorgan.com/